Predicting a Crash: Part Two

In the first part of Predicting a Crash, I identified debt as one of the main drivers of global weakness in the past couple of years. Despite the mountains of debt that brought down the housing market, developed and emerging economies have continued to borrow piling onto record levels of sovereign, household, and corporate debt. At some point, this pyramid will implode taking down the global economy with it. If you don't believe me, refer back to the financial crisis just eight years ago for an example of the crushing effects of too much debt. But the crash of the housing market would be small potatoes compared to what could happen if governments and multinational corporations tumble from the leveraged pedestal from which they rule. In this installment of Predicting the Crash, we'll begin to dissect the debt problems and what companies, governments, and analysts are saying about its implications.

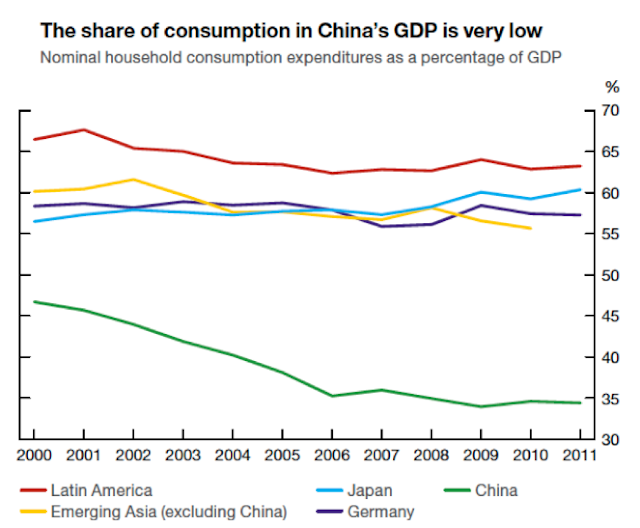

Because of its large growth rates and massive population, China, and its insatiable demand, has quickly become the key driver of global economic expansion since the financial crisis. It's GDP growth rate, which approached 10 percent in the years of the recovery, catapulted the Asian country's total output above the United States. The robust expansion of the Chinese economy is a very optimistic economic prospect promising more demand and consumption of exports from its trade partners and blue chip investments from developed economies looking for a stable way to grow their capital. However, the trends underneath it all finally began to show themselves in late 2015 and early 2016 when stock markets crashed around the globe. The sell-offs were caused by the realization that Chinese stocks had been built up into bubble territory by foreign capital that was unsupported by expansion in domestic Chinese consumption. In a chart from the Bank of Canada's Financial System Review in December of 2012, data shows a declining consumption share of GDP in China leading up to the financial crisis remaining below 35 percent through 2012. This level is extremely low compared to its emerging Asian peers, Latin America, Japan, and Germany.

Since the capital flowing through the hands of Chinese consumers wasn't sufficient in supporting the growth of the Chinese private sector, the firms there looked to its government, local banks, and foreign investors to raise the money. In the most recent Financial System Review report, the Bank of Canada pointed to this chart to summarize the proliferation of outstanding loans in the world's largest producer of goods and services. Ever since the financial crisis caused emergency loans to bail-out the nations company's, debt has continue to build approaching the frightening level of 225 percent of GDP. The weakness that was revealed in August of 2015 toppled these company's share prices but the problem has only gotten worse. In fact, interest on these loans has become the biggest issue as 16 percent of the largest 1,000 Chinese companies "owed more in interest than they earned before tax" according to The Economist. Eventually, weakness and fragility turns into defaults and bankruptcy then soon panic. In the same The Economist article, the author writes, "When the debt cycle turns, both asset prices and the real economy will be in for a shock." It's true. China's debt problem is a ticking time bomb. And we're all exposed.

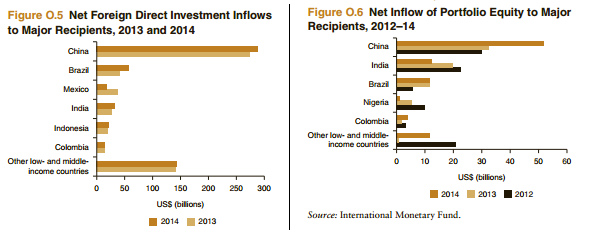

As the emerging economies have quickly become the world's growth leaders, foreign capital has flooded their companies and governments in search for high yield in a low interest rate global economy. China, the fastest growing developing nation, has claimed a large share of the foreign direct investment because if its bullish demographics and stock market. In the World Bank's International Debt Statistics 2016, the report highlights the Chinese share of foreign investment in the charts above. In 2014, the Asian giant absorbed over $260 billion of foreign direct investment. The demand for Chinese debt securities has caused its bond market to grow to $7.5 trillion, "the world's third-biggest," according the The Economist. Instead of the housing market, easy capital egged on by low interest rates is accumulating in the debt heavy companies China. And its government is doing its best to support those investments. The Economist reports that the "$200 billion" was spent to "prop up the stock market" as "$65 billion of bank loans" went bad in the same time period. The kingpin of global growth will attempt to shoulder the debt load going into the future, but foreign investors may be convinced to withdraw their capital as pessimism looms and debt crises in their own countries develop.

Many developed nations, the source of much of the foreign direct investment that finds its way into the hands of China and other emerging economies, find themselves facing debt problems themselves. The growth rate of the economies in the European Union have slowed drastically sometimes struggling to reach a meager 2 percent. As the markets have started to flatten, debt-to-GDP ratios have blossomed in their place. As shown by the chart above, the four most leveraged nations in the EU have seen their debt-to-GDP ratios grow significantly from 2010 to 2014. Greece, a country that has already tested the fragility of the economic unity in the eurozone, is approaching a ratio of almost 200 percent despite austerity measures. The rest of the EU-15 nations are only relatively better compared to the Greece, Portugal, Italy, and Ireland. The average government debt-to-GDP ratio in the European Union is 84.4 percent according to 2014 data, up from 83.2 percent in 2013. Pressure in united Europe will continue to build as each country takes its turn on the brink of a debt crisis. A failure in any one economy could be devastating enough to dissolve the union indefinitely, an outcome that would surely lead to an unraveling of the global economy.

The jaded European nations are not the only developed countries to carry the heavy burden of excessive debt. Japan, notorious for its low growth "Lost Decade," operates on a debt-to-GDP- ratio above 200 percent, the highest of the OECD countries. The nation has been a large contributor to the expansion of the Chinese economy as its established companies poured money into the emerging private sector in the world's most populous region. However, data produced in the latter parts of 2015 revealed a "25.1 percent" drop in Japanese direct investment in China, according to the Global Times. This decline is reported just after the Shanghai Composite index lost much of the growth it experienced in the years before. This is just the first signal of investors finally coming to terms with the weight of the debt load on these two Asian economies. The next step will be the flight of American investors as the first two crashes introduce the taste blood to their trading taste buds. The United States is not a country that has avoided debt problems with a debt-to-GDP-ration of 97 percent and a national debt of almost $20 trillion. The unique relationship that China, as creditor, and United States, as debtor, could eventually crumble if the U.S. proves to be irresponsible with its repayments. Nevertheless, a sovereign debt default in the United States is not likely to be the catalyst in the global crisis that is to come.

In this article, we've identified the frightening debt trend that has consumed the global economy and the stock and bond markets in just about every country. While risk can be found just about anywhere, the overpriced Chinese firms built on loans and foreign capital are the largest current threat. A crisis will most likely start in the bond and stock markets after more bubbles are forced to deflate, crashes that would cause investors and governments to panic. The last thing anyone wants if for debts to be called in, but this nightmare could become a reality if sentiment deteriorates enough. As the world's central banks' hold their fingers on the detonator, reluctant to let go, all eyes turn to them. Since that is the case, I shall turn with them as I continue Predicting a Crash.

Comments

Post a Comment