Fundamental Friday: 10 June 2016

Crude oil: Crude oil fundamentals record a very important move this week in the EIA supply estimates. Domestic production reversed its long downtrend to add 10,000 b/d for a total of 8.745 million b/d. After a thirteen week losing streak, U.S. suppliers finally signaled that are ready to increase output in a recovering environment. While 10,000 b/d will not have a large impact on supply and demand dynamics, it represents a reversal that could heap bearish sentiment onto the markets (if confirmed of course). Stockpiles, though, fell by just over 3 million barrels to end at 1.227 billion for the same week. Because stocks tend to lag production, the new trend of draws on inventories could be in danger.

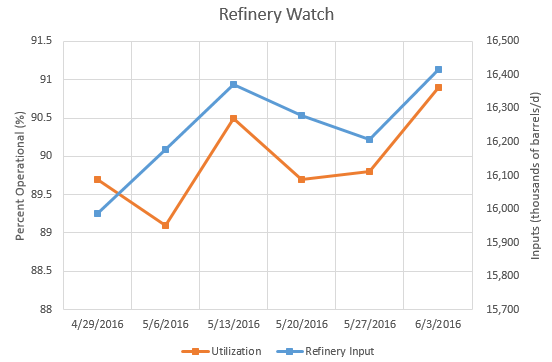

Refineries provided a bullish counter to the increase in production this week. Crude oil inputs jumped 211,000 b/d to 16.417 million b/d, higher than any of the values estimated for the weeks in May. Rig utilization jumped 1.1 percent to 90.9 percent. Some growth in both categories should be expected as refinery operations usually peak in July. Typically, the acceleration weighs on stocks, but a substantial boost in production could cancel out that effect.

After peaking above $51, the WTI spot price fell to about $49.40 on Friday with a five-day gain of 1.4 percent. Brent crude maintained its growth over the $50 mark ending around $50.70 on Friday after a five-day jump of 2.1 percent.

Natural gas: Natural gas fundamentals appear to reflect the expectations of higher consumption in the coming summer months. Underground stockpiles grew by 65 bcf to a total of 2,972 bcf for the week. While the glut continues, smaller increases have allowed the current storage values to approach the historical averages. After this week, natural gas stocks are just 32 percent higher than the 5-year average when it was about 69 percent higher a little over two months ago. Supply fell by 0.4 bcf/d and demand grew 0.8 bcf/d adding to the bullish pressure. The natural gas rig count increased by 3 to 85 as companies start to bring more drills online due to higher prices

This week in petroleum, the Henry Hub futures curve began to form a slight contango pattern with investors expecting prices to rise over the summer. The EIA found a $0.20 difference between the July contract and the expired June contract on May 27th. Last year, the difference was only $0.09. While the summer months usually cause this pattern to develop, this year's futures difference is well above the average. If temperatures continue to rise to above-average levels, the cooling season could instigate a more secure uptrend going into the heating season.

Natural gas Henry Hub spot price grew an impressive 7.55 percent in the past five days after some small gains on Friday brought the price from its peak of $2.617 on Thursday.

Gasoline: Increases in refinery operations have caused a parallel growth in product supplies. Finished gasoline soared to new highs of 25.037 million barrels after a 1.6 million barrel growth in the last week. Component gasoline stocks fell about 600,000 barrels to 214.593 million barrels in conjunction with higher refining rates. Finished gasoline production grew 200,000 b/d to 10.122 million b/d total. Finished gasoline data were well above those recorded for the month May. Product supplied fell about 600,000 b/d to 19.779 million b/d for last week. If the industry expectations are correct, this value, reflecting demand, should increase during the summer driving season.

Gas prices continue to extend their incline into the summer months, something not out of the ordinary according to seasonal analysis. U.S. regular gas prices grew $0.042 to $2.381 per gallon with a consistent trend evident throughout the PADD regions. Diesel fuel prices grew by $0.025 to $2.407 per gallon. The differential between diesel and regular gas prices has shrunk to a new low of $0.026.

Refineries provided a bullish counter to the increase in production this week. Crude oil inputs jumped 211,000 b/d to 16.417 million b/d, higher than any of the values estimated for the weeks in May. Rig utilization jumped 1.1 percent to 90.9 percent. Some growth in both categories should be expected as refinery operations usually peak in July. Typically, the acceleration weighs on stocks, but a substantial boost in production could cancel out that effect.

After peaking above $51, the WTI spot price fell to about $49.40 on Friday with a five-day gain of 1.4 percent. Brent crude maintained its growth over the $50 mark ending around $50.70 on Friday after a five-day jump of 2.1 percent.

Natural gas: Natural gas fundamentals appear to reflect the expectations of higher consumption in the coming summer months. Underground stockpiles grew by 65 bcf to a total of 2,972 bcf for the week. While the glut continues, smaller increases have allowed the current storage values to approach the historical averages. After this week, natural gas stocks are just 32 percent higher than the 5-year average when it was about 69 percent higher a little over two months ago. Supply fell by 0.4 bcf/d and demand grew 0.8 bcf/d adding to the bullish pressure. The natural gas rig count increased by 3 to 85 as companies start to bring more drills online due to higher prices

This week in petroleum, the Henry Hub futures curve began to form a slight contango pattern with investors expecting prices to rise over the summer. The EIA found a $0.20 difference between the July contract and the expired June contract on May 27th. Last year, the difference was only $0.09. While the summer months usually cause this pattern to develop, this year's futures difference is well above the average. If temperatures continue to rise to above-average levels, the cooling season could instigate a more secure uptrend going into the heating season.

Natural gas Henry Hub spot price grew an impressive 7.55 percent in the past five days after some small gains on Friday brought the price from its peak of $2.617 on Thursday.

Gasoline: Increases in refinery operations have caused a parallel growth in product supplies. Finished gasoline soared to new highs of 25.037 million barrels after a 1.6 million barrel growth in the last week. Component gasoline stocks fell about 600,000 barrels to 214.593 million barrels in conjunction with higher refining rates. Finished gasoline production grew 200,000 b/d to 10.122 million b/d total. Finished gasoline data were well above those recorded for the month May. Product supplied fell about 600,000 b/d to 19.779 million b/d for last week. If the industry expectations are correct, this value, reflecting demand, should increase during the summer driving season.

Gas prices continue to extend their incline into the summer months, something not out of the ordinary according to seasonal analysis. U.S. regular gas prices grew $0.042 to $2.381 per gallon with a consistent trend evident throughout the PADD regions. Diesel fuel prices grew by $0.025 to $2.407 per gallon. The differential between diesel and regular gas prices has shrunk to a new low of $0.026.

Comments

Post a Comment