Fundamental Friday: 24 June 2016

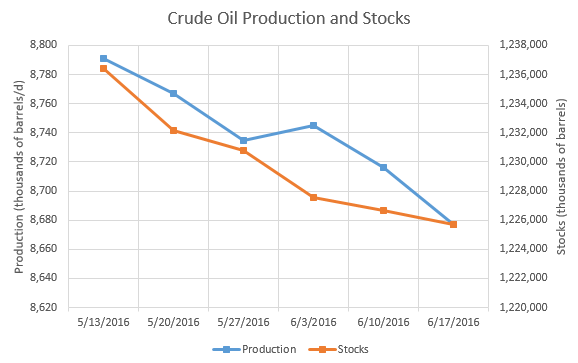

Crude oil: Crude oil fundamentals are reacting bullishly to the spike in refining this summer. Domestic production fell 39,000 b/d to 8.677 million b/d approaching another significant milestone at 8.5 million b/d. Since the beginning of the year, U.S. producers have cut 542,000 b/d worth of production as the squeeze on supply continues despite the stabilization of oil prices. Crude oil stockpiles continued their decline as well. With a drop of about 900,000 barrels, last week stockpiles were reported at 1.225 billion barrels. For the year, stocks are up about 48 million barrels but have declined in the past two months at a rate of about 13 million barrels.

Refinery data spiked to new highs this week as upstream operations heat up with the temperatures. Refinery inputs grew by 190,000 b/d to 16.505 million b/d reaching a new peak for the year. So far, June averages are well above the earlier 2016 months. Compared to last year, this week's refinery inputs are just 27,000 b/d lower, on par with the season average. Utilization peaked this week as well jumping 1.1 percent to 91.3 percent. Utilization data, compared to what it was last year, is 2.7 percent lower hinting at higher refinery input to come later in the summer.

WTI and Brent spot prices traded turbulently this week with Brexit weighing at the end of the week. The declines on Friday helped solidify the $50 mark as a potential resistance going forward. WTI settled at $47.50, and Brent settled at $49.00.

Natural gas: Natural gas supply and demand trends extend the pattern that has developed in the past couple of months. Underground stockpiles of natural gas jumped 62 bcf to another new high of 3103 bcf. The rig count jumped at the highest rate in awhile, up 4 rigs to a total of 90 for this week. The growth in rig operation is most likely caused by an even stronger jump in demand. The EIA estimates a 0.3 bcf/d increase in supply for this week. The estimate for demand growth is 1.8 bcf/d completely offsetting and overwhelming the corresponding shifts in supply.

In the weekly report on natural gas fundamentals, the EIA discusses the pace at which the 2016 summer season is growing. Last week's peak above 3,000 bcf marked the earliest date at which this level was reached over the past 20 years. In 2012, supply reached this point by June but was still below 2016 fundamental data. Projections have the 2016 summer injection season ending with stockpiles just above 4,000 bcf, a point never reached before.

Henry Hub spot prices continued their impressive streak of gains despite losses on Friday. A 5-day gain of 0.84 percent adds on to three-month growth of 23.99 percent.

Gasoline: Gasoline supply data reflected the expectation of more consumption to come in the next two months. Finished motor gasoline production grew by 580,000 b/d to end at a six-week high of 10.289 million b/d. As a result, finished motor gasoline stockpiles grew as well adding just under 1.5 million barrels for a total of 25.016 million b/d last week. Component stocks fell by 800,000 barrels to 212.615 million barrels. These data confirm the expectation that higher consumption is imminent. Product supplied contradicted the assumed trend falling 830,000 b/d to 20.010 million b/d after a peak the week before.

Regular and diesel gas prices reversed this week after a long streak of gains. Regular gas fell by $0.046 to $2.353 per gallon with declines across all regions. Diesel gas prices fell as well down $0.005 to $2.426 per gallon with mixed data across the regions. The drop in prices may have been a reaction to higher product supply corresponding with flat demand.

Refinery data spiked to new highs this week as upstream operations heat up with the temperatures. Refinery inputs grew by 190,000 b/d to 16.505 million b/d reaching a new peak for the year. So far, June averages are well above the earlier 2016 months. Compared to last year, this week's refinery inputs are just 27,000 b/d lower, on par with the season average. Utilization peaked this week as well jumping 1.1 percent to 91.3 percent. Utilization data, compared to what it was last year, is 2.7 percent lower hinting at higher refinery input to come later in the summer.

WTI and Brent spot prices traded turbulently this week with Brexit weighing at the end of the week. The declines on Friday helped solidify the $50 mark as a potential resistance going forward. WTI settled at $47.50, and Brent settled at $49.00.

Natural gas: Natural gas supply and demand trends extend the pattern that has developed in the past couple of months. Underground stockpiles of natural gas jumped 62 bcf to another new high of 3103 bcf. The rig count jumped at the highest rate in awhile, up 4 rigs to a total of 90 for this week. The growth in rig operation is most likely caused by an even stronger jump in demand. The EIA estimates a 0.3 bcf/d increase in supply for this week. The estimate for demand growth is 1.8 bcf/d completely offsetting and overwhelming the corresponding shifts in supply.

In the weekly report on natural gas fundamentals, the EIA discusses the pace at which the 2016 summer season is growing. Last week's peak above 3,000 bcf marked the earliest date at which this level was reached over the past 20 years. In 2012, supply reached this point by June but was still below 2016 fundamental data. Projections have the 2016 summer injection season ending with stockpiles just above 4,000 bcf, a point never reached before.

Henry Hub spot prices continued their impressive streak of gains despite losses on Friday. A 5-day gain of 0.84 percent adds on to three-month growth of 23.99 percent.

Gasoline: Gasoline supply data reflected the expectation of more consumption to come in the next two months. Finished motor gasoline production grew by 580,000 b/d to end at a six-week high of 10.289 million b/d. As a result, finished motor gasoline stockpiles grew as well adding just under 1.5 million barrels for a total of 25.016 million b/d last week. Component stocks fell by 800,000 barrels to 212.615 million barrels. These data confirm the expectation that higher consumption is imminent. Product supplied contradicted the assumed trend falling 830,000 b/d to 20.010 million b/d after a peak the week before.

Regular and diesel gas prices reversed this week after a long streak of gains. Regular gas fell by $0.046 to $2.353 per gallon with declines across all regions. Diesel gas prices fell as well down $0.005 to $2.426 per gallon with mixed data across the regions. The drop in prices may have been a reaction to higher product supply corresponding with flat demand.

Comments

Post a Comment