Unemployment Claims and Cuts Slow But a Long Way From Normal

Economic Report Monitor #37

June 4th, 2020

|

| From The Real Economy Blog |

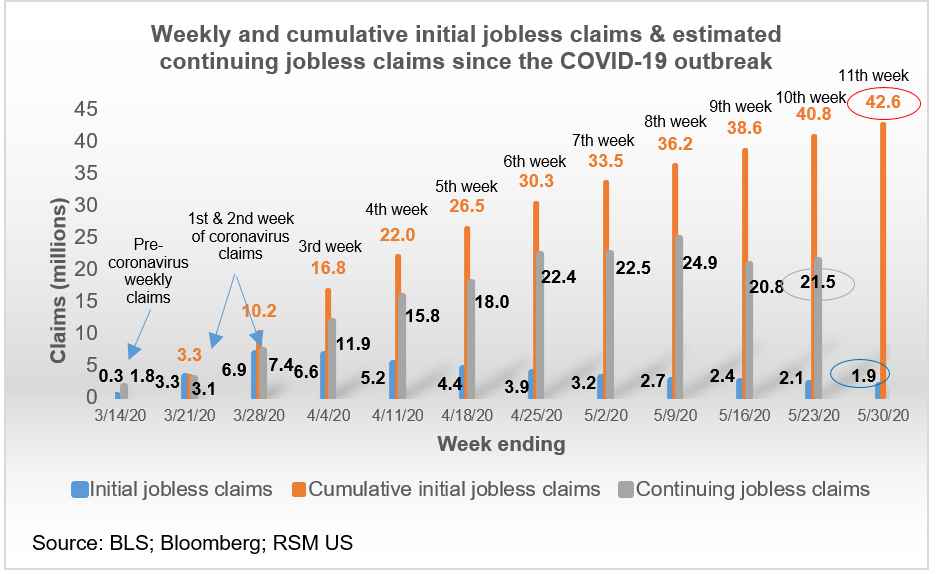

Another report on unemployment was released by Challenger Gray & Christmas documenting the job cuts in May. While down 40.8% from April, the total of 397,016 was the 2nd highest monthly total in the history of the data series. Year-to-date job cuts are up 389.5% at 1,414,828 after COVID-19 causes 984,073 job cuts alone. The devastation to payrolls is 9.8% higher than in the height of the Great Recession in 2009. Drilling down into the data, the trends become predictable. Both entertainment/leisure and retailers were hit the hardest in may seeing 163,680 and 151,416 job cuts respectively. The pain continued for non-essential businesses in May, but it seems that April was the bottom of the job cut crisis. It will be interesting to see if the number of job cuts reverts to its normal pace, or if another set of job cuts looms as businesses are threatened to cut wages on much lower revenue and utilization.

That lower utilization was evident in the April international trade report from the Bureau of Economic Analysis. Exports were devastated, down -20.5% as foreign demand dried up. Closures on the domestic front also squashed demand for outside goods and services as imports fell -13.7%. However, since the export drop was deeper, the deficit ballooned 16.7%, reversing its trend of shrinking over the past year. Goods exports fell across the board with capital goods falling -$10.1 billion, industrial supplies falling -$9.1 billion, and automobile vehicles, parts, and engines falling -$7.4 billion. Automotive imports fell the most on the other hand, down -$14.6 billion, as durable goods demand dried up. Other import categories saw smaller drops likely because of China's resumption of exports. In this same period that total imports fell steeply, the deficit with China increased by almost 50% to $26.0 billion as the US imported $11.0 billion more from the Asian country in April.

The disruption in the durable goods market was evident again in the 2020 Q1 productivity and costs report. Overall, productivity fell -0.9%, a minor shift, as output dropped -6.5% while hours worked fell -5.6%. However, once the data is split, the difference describes how two different economies have seen isolated effects during the COVID-19 outbreak. Both durable and non-durable goods industries saw similar hours worked, -6.9% and -6.1% respectively, but their outputs (and thus productivity) were miles apart. Durable output dropped -10.2% as employers reduced capacity but tried to keep on employees in hopes of a short-term effect. For that reason, unit labor costs shot up to 11.4% and productivity fell -3.5%. On the other hand, non-durables (especially of products that were being stockpiled) were forced to maintain output while also reducing employment to meet social distancing standards. That combination lead to a smaller drop in output, -2.0% and a large increase in productivity up 4.3%. Yet another report shows that these two segments of the economy are experiencing different effects from the COVID-19 outbreak and that the public health inspired financial crisis differs vastly from the crisis in 2008-2009.

Comments

Post a Comment