How a Pandemic Became a Global Financial Crisis

On March 18th, 2020, the US Congressional Research Service (CRS) issued a report briefly summarizing its forecasts for the economic effects of COVID-19. The disease, originating in the Wuhan province of China, has sent the world in a panic as its high transmission rate and mortality rate threaten the global population. The response to the disease, social distancing and temporary closing of economies, will pose a threat to already feeble global growth.

The Organization for Economic Cooperation and Development (OECD) has noted these effects in a downward revision of global economic growth. In the best-case scenario, where the effects of the virus peak in Q1, growth in 2020 will experience a relatively small drop of -0.5 percent to 2.4 percent for the year; however, if the virus effects peak later, the drop could be as much as -1.5 percent to 1.4 percent. Of course, this has caused panic in financial markets as investors traded equities volatilely and crowded into bonds sending the 10-year Treasury yield below 1 percent for the first time ever.

The OECD has slashed growth forecasts across the globe. Here are some things to note:

The Organization for Economic Cooperation and Development (OECD) has noted these effects in a downward revision of global economic growth. In the best-case scenario, where the effects of the virus peak in Q1, growth in 2020 will experience a relatively small drop of -0.5 percent to 2.4 percent for the year; however, if the virus effects peak later, the drop could be as much as -1.5 percent to 1.4 percent. Of course, this has caused panic in financial markets as investors traded equities volatilely and crowded into bonds sending the 10-year Treasury yield below 1 percent for the first time ever.

The OECD has slashed growth forecasts across the globe. Here are some things to note:

- The largest slowdowns are likely to occur in the Asian giants China and India. Their status of large population centers and emerging economies makes them especially vulnerable. Of course, China also contains the epicenter of the outbreak.

- As expected, emerging economies are projected to suffer more as they are likely to be more affected by the weakening of the slowdown in the global supply chain (which has already been seen by the effects of the US-China trade dispute).

- Large developed nations, Germany and the US are expected to see minimal drops of -0.1% in 2020 with 2021 growth safe from the virus.

- The United Kingdom is expected to see compounding negative effects from Brexit which occurred at the end of January.

- Countries like Saudi Arabia and Russia may see further, more lasting risks to growth as the price of oil plummeted in early March.

- The initial expectation of the OECD is that the virus effects will be temporary. In many 2021 growth estimates, economies are expected to stabilize and in some cases expand faster than they fell. This trend in expectations speaks to cautious optimism that is not reflected in global markets and policymakers' responses.

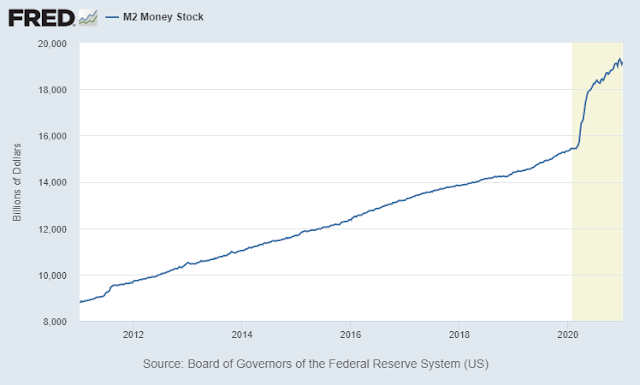

The lack of positive and sell-off in the stock market appears similar to the 2008 global financial crisis. Both crises saw liquidity squeezed putting short-term markets in danger. The initial shocks were in 2008 and 2020 were different, but in both cases, a demand shock has caused expected revenue to drop especially in specific industries. The Federal Reserve has stepped in to relieve financial institutions again with over $1 trillion in Treasury purchases and 150 basis points of rate cuts. In 2008, Troubled Asset Relief Program (TARP) and Term Asset Back Security (TALF) were announced to save distressed securities, and the Fed cut from 5 percent down to 0-0.25 percent. Those programs were successful in quieting the storm that was the financial markets in 2009, but they couldn't fend off a painfully slow recovery. Will the global economy see a similarly slow recovery in response to the damage of COVID-19?

The answer may lie in a key difference between the two crises. The current COVID-19 pandemic has created concurring demand and supply shocks that threaten to disrupt economic growth while the global financial crisis was bereft of the physical hindrance to global supply. The CRS points out that "unlike the 2008 crisis response, which involved liquidity and solvency-related policy measures to get people spending again, the current crisis is related to the amount of operating capital in the economy." It also points out that problems like these are only slightly affected by monetary policy and require a more direct fiscal stimulus.

Another troubling aspect of the proposed economic collapse caused by COVID-19 is that globalized supply chains of goods and services threaten to spread financial trouble even if a country is not directly affected by the virus (much like how the interconnectedness of the global financial system in 2008 caused local problems to become much bigger). With China being the epicenter of the outbreak and being a crucial part of the global trade infrastructure, its lockdown has "created larger supply issues as firms experienced delays in supplies in intermediate and finished goods through supply chains." As mentioned before, the combination of these supply shocks and local demand shocks due to each country's response to containing the virus has created liquidity problems for cash light firms.

As mentioned above, emerging economies are expected to be more sensitive to the supply and demand shocks as often they rely on the global supply chain to bolster growth. The COVID-19 outbreak effects have already forced a massive capital outflow from those economies, more than double the size of the 2008 global financial crisis. Certain countries have seen their currencies depreciate heavily as the rush to dollars creates deflationary shocks for the currencies of Mexico (-21.0 percent YTD), Russia (-20.5 percent), Turkey (-8.5 percent), and several others.

The response of policymakers across the globe has been swift and decisive. The United States alone is looking to spend upwards of $2 trillion on a stimulus package to provide relief after it has deployed emergency lending facilities and seen the Federal Reserve cut rates to 0 percent. The CRS report includes a comprehensive list of global monetary and fiscal actions taken in an appendix starting on page 18. As of March 21st, several of these countries have only reported a couple hundred reported cases or even less, but the economic effects are still likely to be felt, there is no doubt about that. The only question that remains is whether or not these actions will be enough.

The answer may lie in a key difference between the two crises. The current COVID-19 pandemic has created concurring demand and supply shocks that threaten to disrupt economic growth while the global financial crisis was bereft of the physical hindrance to global supply. The CRS points out that "unlike the 2008 crisis response, which involved liquidity and solvency-related policy measures to get people spending again, the current crisis is related to the amount of operating capital in the economy." It also points out that problems like these are only slightly affected by monetary policy and require a more direct fiscal stimulus.

Another troubling aspect of the proposed economic collapse caused by COVID-19 is that globalized supply chains of goods and services threaten to spread financial trouble even if a country is not directly affected by the virus (much like how the interconnectedness of the global financial system in 2008 caused local problems to become much bigger). With China being the epicenter of the outbreak and being a crucial part of the global trade infrastructure, its lockdown has "created larger supply issues as firms experienced delays in supplies in intermediate and finished goods through supply chains." As mentioned before, the combination of these supply shocks and local demand shocks due to each country's response to containing the virus has created liquidity problems for cash light firms.

As mentioned above, emerging economies are expected to be more sensitive to the supply and demand shocks as often they rely on the global supply chain to bolster growth. The COVID-19 outbreak effects have already forced a massive capital outflow from those economies, more than double the size of the 2008 global financial crisis. Certain countries have seen their currencies depreciate heavily as the rush to dollars creates deflationary shocks for the currencies of Mexico (-21.0 percent YTD), Russia (-20.5 percent), Turkey (-8.5 percent), and several others.

The response of policymakers across the globe has been swift and decisive. The United States alone is looking to spend upwards of $2 trillion on a stimulus package to provide relief after it has deployed emergency lending facilities and seen the Federal Reserve cut rates to 0 percent. The CRS report includes a comprehensive list of global monetary and fiscal actions taken in an appendix starting on page 18. As of March 21st, several of these countries have only reported a couple hundred reported cases or even less, but the economic effects are still likely to be felt, there is no doubt about that. The only question that remains is whether or not these actions will be enough.

Comments

Post a Comment