Coronavirus Economic Impact, Wells Fargo Perspectives

Over the past month, the coronavirus has taken the world by storm. First appearing in the world's largest economy, the virus grew rapidly, eventually stalling activity in Chinese cities with populations in the millions. Until recently, the threat has remained there, but now with infections sprouting in every continent, concerns that the spreading of COVID-19 could turn into a pandemic. Assessing the economic impact will be paramount for businesses and goverments who want to reestablish certainty. Wells Fargo is one of many major organizations trying to bring its own economic perspective to the situation. In several pieces over January and February, it has sought to bring its own perspective to coronavirus economic developments.

Some of the best coverage has come from Wells Fargo which has published some pieces on how the coronavirus could disrupt markets. A January 22nd piece started a trail of research when the virus had infected about 400 individuals across 6 different countries and only 9 fatalities on record. The authors suggested the outbreak looked similar to SARS but with a lower fatality rate. They opined the new coronavirus shouldn't have more than a $40 billion effect (an estimate for the SARS impact), and for the United States, "it is unlikely that the current outbreak will have any material effect on the macroeconomy, at least not at this time." However it does note the impact SARS had on the Taiwanese and Canadian economies.

Expounding on the US impact, another report written on January 27th suggests that if the coronavirus outbreak continues to mirror the SARS outbreak, an impact on consumer sentiment will not materially effect consumer spending. Air transportation spending ended up being the segment that was most affected, likely because of travel advisories issued. Durable good spending also appeared sensitive, but it bounced back quickly. Overall, though, the consumer would keep spending, and with a coronavirus trend that tracked SARS, one might expect "that U.S. consumer spending will likely not be materially affected by the Wuhan coronavirus."

On January 28th, Wells Fargo turns its focus to US factory production. The authors choose not to use SARS for its short case study because it coincides with the beginning Iraq War. Instead, it points out disruptions to motor vehicle assemblies after the earthquake in Japan that caused the Fukushima nuclear disaster. There's no doubt that in 2018-2019 the US relies more on Chinese imports, and though most of those imports are consumer goods, two industries stick out as vulnerable, computer & electrical equipment and machinery. While these segments might feel more severe pain, "the U.S. economy has become less reliant on manufacturing, so even if the sector were to fall under pressure, it would be unlikely to cause a U.S. recession."

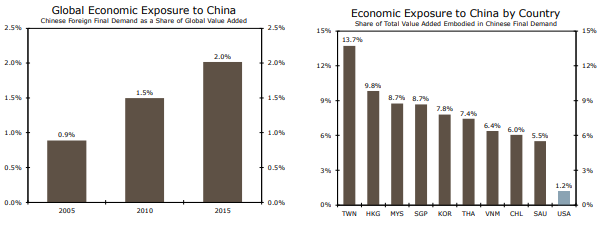

By February 4th, the report takes a look at the global impact of an infected China. Previously reports compared SARS impact economically, and the same applies. Wells Fargo notes that when SARS hit China in 2005, the Asian giant's share of global final demand was 0.9 percent. In 2015, that value had more than doubled to 2.0 percent. China's closest neighbors are likely to feel more pain. Specifically, Taiwan, Hong Kong, Malaysia, Singapore, and South Korea see China as more than 7 percent of its final demand. Of course, as the virus worsened, weak economic performance wouldn't be the only infection that jumped from China to its direct neighbors. In this report, Wells Fargo suggested a limited economic connection between the US and China relative to other Asian countries with China only accounting for 1.2 percent of US final demand and only 10 percent of US's final demand coming from foreign entities. A separate report on the same day updated Walls Fargo 2020 GDP to be 5.5 percent, down from 5.9 percent.

While the impact to the United States seems to be downplayed in the previous report, a February 11th analysis breaks down where the pain is most likely to be felt.

By the end of the month, Europe now looked to be in direct danger of the virus as an outbreak occurred in Italy. The Eurozone economy, growing just 0.9 percent in 2019 Q4, was already struggling with deflation and slow growth. Italy, which accounts for about 15 percent of the area's GDP growth, is likely to enter a lockdown state with other European countries taking similar precautions to stop an outbreak before it occurs. Wells Fargo dropped its Eurozone GDP estimates from 0.2 percent (already accounting for China slowdown) to 0.1 percent.

The situation has precipitated to the point where policy action across the globe has become expected. However, the unique circumstances related to the coronavirus outbreak calls into question the efficacy of stimulus measures. In a February 26th report, Wells Fargo pointed out that the market had already priced in a 50 basis point rate cut (which it would get in emergency form on March 3rd). The European Central Bank, bereft of monetary tools, signaled for fiscal stimulus to be employed instead. Both measures would probably increase consumer and business spending, but they fail in the realization that low rates won't matter if workers and consumers are too sick to participate in the economy.

Wells Fargo's perspective of the economic impact of the coronavirus seemed to intensify with the progression of the outbreak. The fluid discussion reflects how expectations of the effects of the coronavirus have evolved and continue to evolve in the opening months of 2020. The increased uncertainty has impacted financial markets already as expectations remain volatile and the situation develops.

Some of the best coverage has come from Wells Fargo which has published some pieces on how the coronavirus could disrupt markets. A January 22nd piece started a trail of research when the virus had infected about 400 individuals across 6 different countries and only 9 fatalities on record. The authors suggested the outbreak looked similar to SARS but with a lower fatality rate. They opined the new coronavirus shouldn't have more than a $40 billion effect (an estimate for the SARS impact), and for the United States, "it is unlikely that the current outbreak will have any material effect on the macroeconomy, at least not at this time." However it does note the impact SARS had on the Taiwanese and Canadian economies.

On January 28th, Wells Fargo turns its focus to US factory production. The authors choose not to use SARS for its short case study because it coincides with the beginning Iraq War. Instead, it points out disruptions to motor vehicle assemblies after the earthquake in Japan that caused the Fukushima nuclear disaster. There's no doubt that in 2018-2019 the US relies more on Chinese imports, and though most of those imports are consumer goods, two industries stick out as vulnerable, computer & electrical equipment and machinery. While these segments might feel more severe pain, "the U.S. economy has become less reliant on manufacturing, so even if the sector were to fall under pressure, it would be unlikely to cause a U.S. recession."

By February 4th, the report takes a look at the global impact of an infected China. Previously reports compared SARS impact economically, and the same applies. Wells Fargo notes that when SARS hit China in 2005, the Asian giant's share of global final demand was 0.9 percent. In 2015, that value had more than doubled to 2.0 percent. China's closest neighbors are likely to feel more pain. Specifically, Taiwan, Hong Kong, Malaysia, Singapore, and South Korea see China as more than 7 percent of its final demand. Of course, as the virus worsened, weak economic performance wouldn't be the only infection that jumped from China to its direct neighbors. In this report, Wells Fargo suggested a limited economic connection between the US and China relative to other Asian countries with China only accounting for 1.2 percent of US final demand and only 10 percent of US's final demand coming from foreign entities. A separate report on the same day updated Walls Fargo 2020 GDP to be 5.5 percent, down from 5.9 percent.

While the impact to the United States seems to be downplayed in the previous report, a February 11th analysis breaks down where the pain is most likely to be felt.

- Clearly, port traffic is a main concern for the West Coast as states like California, Oregon, Nevada, Idaho, and Washington see Chinese exports and imports as 3 percent or more of their GDP. More subtlety and as a result of China's further entanglement in global trade, East Coast ports like NY-NJ, Savannah, GA, and Charleston, SC have seen Chinese volumes increase as well.

- Supply chain disruptions in key industries like computer and electronics, machinery, and fabricated metals. About 20 percent of the West Coast's computer and electronics industry’s inputs are imported from China putting those states in danger of an economic slowdown. Auto manufacturing in the South and Midwest also look to be threatened as plants in states like Michigan, Indiana, Kentucky, and Tennessee sit exposed to China's Hubei province (one of China's largest auto production centers) slowdown.

- In a more direct way, lower Chinese oil demand will lead to faltering oil prices. As observed before, oil price struggles impact how Texas, Oklahoma, and other Southwest states perform economically as energy companies decrease capital spending.

- A final mention goes to the impact on Chinese tourism to the US which brought $17 billion in 2018. Those tourism dollars were spent in only a few markets like Los Angeles and San Francisco (37 percent), New York (25 percent), and Los Vegas, Boston, or Washington D.C. (27 percent).

The next day on February 12th, Wells Fargo admits coronavirus economic impact "now looks likely to be greater than the SARS outbreak in

2003." With effects likely to be worse, will factories be ready with excess inventory to survive Chinese supply disruptions? The answer is unclear, but the report notes that manufacturing and wholesale inventories were noticeably higher in 2019 than in 2003. Wells Fargo continues on this topic on February 18th asserting similar conclusions, "High levels of input inventories gives production in most American industries some cushion

against supply chain disruptions from China. That does not mean the current virus outbreak,

however, will not have a bearing on overall GDP growth."

By the end of the month, Europe now looked to be in direct danger of the virus as an outbreak occurred in Italy. The Eurozone economy, growing just 0.9 percent in 2019 Q4, was already struggling with deflation and slow growth. Italy, which accounts for about 15 percent of the area's GDP growth, is likely to enter a lockdown state with other European countries taking similar precautions to stop an outbreak before it occurs. Wells Fargo dropped its Eurozone GDP estimates from 0.2 percent (already accounting for China slowdown) to 0.1 percent.

The situation has precipitated to the point where policy action across the globe has become expected. However, the unique circumstances related to the coronavirus outbreak calls into question the efficacy of stimulus measures. In a February 26th report, Wells Fargo pointed out that the market had already priced in a 50 basis point rate cut (which it would get in emergency form on March 3rd). The European Central Bank, bereft of monetary tools, signaled for fiscal stimulus to be employed instead. Both measures would probably increase consumer and business spending, but they fail in the realization that low rates won't matter if workers and consumers are too sick to participate in the economy.

Wells Fargo's perspective of the economic impact of the coronavirus seemed to intensify with the progression of the outbreak. The fluid discussion reflects how expectations of the effects of the coronavirus have evolved and continue to evolve in the opening months of 2020. The increased uncertainty has impacted financial markets already as expectations remain volatile and the situation develops.

Comments

Post a Comment