The Federal Reserve Decides to Diet

In a press conference on April 5th, 2017, Federal Reserve officials announced their desire to start reducing the size of the Federal Reserve's balance sheet this year. Since the financial crisis in 2008, the size balance sheet has grown to $4.5 trillion worth of bonds and other assets bought up during the period of quantitative easing following the crash of the financial system. In the latest Fed minutes voiced this idea saying, "Provided that the economy continued to perform about as expected, most participants anticipated that gradual increases in the federal funds rate would continue and judged that a change to the Committee's reinvestment policy would likely be appropriate later this year." Since 2009, the members of the Federal Reserve have used various techniques to maintain loose policy as the economy reflated. Lately, though, these mouthpieces have been used to institute a "normalization" policy that will allow interest rates to rise while keeping intentions expansionary.

The chart above shows different asset classes within the Fed's balance sheet accounting for general securities, securities purchased through liquid facilities, and securities purchased to support specific institutions. Growth in the last two was only significant during the financial crisis and was quickly wound down when financial markets return to normal. The assets from credit facilities included purchases by the Term Action Credit, Commercial Paper Funding, Central Bank Liquidity Swaps, and Term Asset-Backed Securities Loan programs. These "liquid facilities" were put in place to create demand in the markets for mortgage-backed securities (MBS), commercial paper (CP), and currency, in particular, the dollar. Even though these programs have been largely inactive since 2010, they ushered in a long period of quantitative easing.

The correlation between the growth in the Federal Reserve's balance sheet and the performance of both long and short term Treasury and corporate bonds is quite strong. Using SHY (Short-term Treasuries), IEF (Long-term Treasuries), CSJ (Short-term corporate), and CLY (Long-term corporate) price trends, a connection can be made between the return of these exchange traded funds and the expansion of the Federal Reserve's balance sheet. With correlation coefficients above 0.80, a strong positive correlation is confirmed at a statistically significant level. The corporate bond ETFs saw correlations that were a bit stronger with the correlation coefficient of CSJ, the fund following short-term corporate bonds, recording an R-squared value of 0.93. From this analysis, one can expect these funds to underperform when the Federal Reserve begins the unwinding process. As interest rates and bond yields start to rise, prices will fall, and this trend will be accelerated with the Federal Reserve reducing demand in those markets. With the speech having reintroduced the issue, market expectations should start to affect the changes in the bond market, and a reaction will be evident soon enough.

The article and charts were written in Python in an IPython Notebook. You can download the code here: .py .ipynb

|

| from Federal Reserve |

In 2007, arguably the last year of the period called "The Great Moderation," the Federal Reserve's balance sheet was below $1 trillion and consisted of mostly Treasury assets used to manipulate interest rates through open market operations. As the crisis unfolded, Fed Chairman Ben Bernanke and Treasury Secretary Hank Paulson saw it necessary for the United States' central bank to buy up the assets that had become worthless due to mortgage defaults. This unconventional intervention in the financial markets, called "quantitative easing," slowed to a stop in the early 2010's, but by then, the balance sheet had more than tripled. The average increase per year over the past 10 years was about 25 percent.

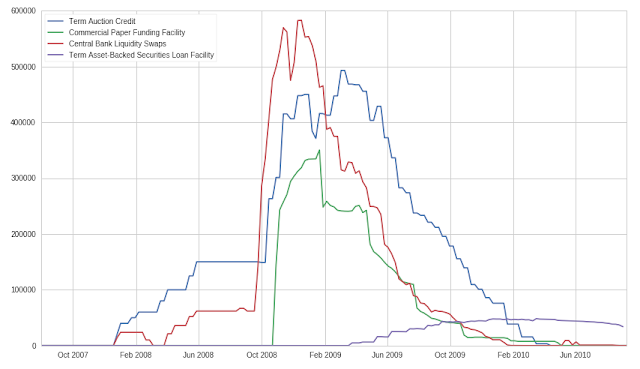

Looking closer at the 3 year period around the financial crisis reveals a jump in the activity of the liquid facilities that spurred the growth of the Federal Reserve's balance sheet. Two of these programs saw activity before the fall of Lehman Bros in late 2008, the Term Auction Credit (TAF) program and Central Bank Liquidity Swaps. These credit facilities are no longer being used and haven't been since around 2011, but some of the assets still linger on the balance sheet. Most of those assets are loans supplied by these programs (mostly Term Asset-Backed Securities Loan Facility) in which credit facilities were provided for banks with the MBS put up as collateral.

Unwinding a balance sheet of an assortment of $4.5 trillion assets is a very complicated process. With such careful decisions being made about interest rate hikes, the Federal Reserve has shown how important they think timing is in monetary policy. Their stance will be no different this time around. In an article from the Brookings Institute, Ben Bernanke refers to the Fed's most recent discussion of how to unwind the balance sheet released in September 2014 suggesting that, "the balance sheet will ultimately be reduced, not by sales of assets that the Fed holds, but by ceasing or phasing out the Fed’s current practice of replacing or rolling over maturing assets (“reinvestment”)." This makes sense. Federal Chairwoman Janet Yellen has assured us that she doesn't intend to shock the markets with what her board does, and so far, she has not disappointed. With that in mind, investors shouldn't be expecting a smaller Fed for a while. In fact, the process may end up being a non-issue with conventional monetary policy changes always occupying the spotlight. The Federal Reserve hasn't actually decided on how to go about the unwinding yet, but investors can expect a very tame approach in the end.

During the press conference in April, the stock market saw a reversal in the day's trading reflecting a bearish response to the unwinding balance sheet. Although the process will be gradual, there will still be fundamental adjustments in financial markets. Investors can expect most of these adjustments to be made in the bond and short-term lending markets with equities being less affected. If anything, the effects of an unwinding balance sheet will be harmonious with the Fed's plan of slowly increasing interest rates, both long and short term.

|

| from Quantopian |

The correlation between the growth in the Federal Reserve's balance sheet and the performance of both long and short term Treasury and corporate bonds is quite strong. Using SHY (Short-term Treasuries), IEF (Long-term Treasuries), CSJ (Short-term corporate), and CLY (Long-term corporate) price trends, a connection can be made between the return of these exchange traded funds and the expansion of the Federal Reserve's balance sheet. With correlation coefficients above 0.80, a strong positive correlation is confirmed at a statistically significant level. The corporate bond ETFs saw correlations that were a bit stronger with the correlation coefficient of CSJ, the fund following short-term corporate bonds, recording an R-squared value of 0.93. From this analysis, one can expect these funds to underperform when the Federal Reserve begins the unwinding process. As interest rates and bond yields start to rise, prices will fall, and this trend will be accelerated with the Federal Reserve reducing demand in those markets. With the speech having reintroduced the issue, market expectations should start to affect the changes in the bond market, and a reaction will be evident soon enough.

The article and charts were written in Python in an IPython Notebook. You can download the code here: .py .ipynb

Comments

Post a Comment