Is There a Bear in the Auto Industry?

A fresh new set of auto sales data has come out in the beginning of August detailing the past month's activity in the buying and selling of motor vehicles. As expected, auto stocks traded lower when the disappointing results were revealed. According to Reuters, shares of General Motor (GM), Fiat Chrysler (FCHA), and Ford (F) traded more that 3 percent lower last week. Reports of March light vehicle sales at about 16.6 million where analyst expectations had drifted slightly above 17 million. Since the financial crisis, automakers have enjoyed a steep expansion in auto sales, but in the past couple of months, that expansion has stopped.

In 2011, a global auto industry exchange traded fund (CARZ) was created to follow the price movement of some of the largest automobile companies in the world. GM and Ford account for over 15 percent of the fund's holdings with Toyota and Honda (both of which rely on U.S. demand) making the ETF very sensitive to auto sales in the United States. After its birth in 2011, CARZ saw a steep incline in its price as light vehicle sales grew steadily. As demand in the industry started to show some slack, the price dipped in 2015 and early 2016. The current dive in auto consumption has CARZ down about 4.7 percent in the last 20 trading days.

With sales starting to slow, there has been an incline in inventory that has left the U.S. auto suppliers in a pickle. Overall, production and imports of cars need to be falling to keep the industry in equilibrium in order to maintain a stable price. Domestic production, in the past 12 months, has fallen just over 14.3 percent while the declines in imports from Canada and Mexico are less significant (and very volatile). This conveys an interesting political signal that suggests Trump's domestic manufacturing goals. After demanding U.S. auto companies to move their manufacturing bases inside the country in his first days as the President, these initial data suggest his protests have been futile. Another interesting observation is to note that inventories haven't seen as significant a move as U.S. production has in the last two years. In fact, inventories have always oscillated within 2.0 and 3.0 with only the latest data peaking about 3.0. The abrupt change in inventories could be a drag on prices which, combined with falling sales, could weigh heavily on automakers' bottom lines.

From the Bureau of Labor Statistics, consumer price index (CPI) data for automobiles, both used and new can be viewed over the past ten years. The CPI for both used and new vehicles has stayed relatively flat from 2012 to now after recovering from a dip caused by a lapse in demand during the financial crisis. For new and used vehicles, prices recovered above their pre-crisis levels in 2010 with more volatility in used car prices. In fact, it seems as if the most of the fluctuations in the overall auto CPI are caused by movement in used CPI. According to this data, automakers selling new cars have enjoyed stable, increasing prices with used car prices inflated beyond their 2007 levels. Perhaps, over the past six years, this phenomenon led consumers to believe that purchasing a new car over a used car was the smarter decision. Thinking practically, used car demand growth post-crisis makes sense because consumers who needed a vehicle might not have had the discretionary funding to purchase an entirely new car. But as demand strengthened, prices rose, and consumers calmed, new auto sales grew. It is possible that now we are observing demand for the "cheaper" used autos grow replacing demand for new autos. This might explain why U.S. production has trailed off while inventories have continued to rise. It is also interesting to note that, according to Reuters, consumer discounts were $441 higher per vehicle than a year ago, a sign that companies were trying to compete with cheaper used cars on the market.

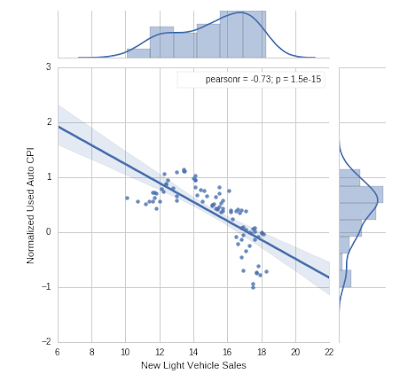

Post-crisis, an interesting trend in used car CPI and light vehicle sales data can be identified. Using data from 2010 on, one can observe a strong negative correlation between used car CPI and new light vehicle sales as reported by the Bureau of Labor Statistics. With a correlation coefficient of -0.73 and a statistically significant p-value, the data suggests that as used cars get more expensive relative to new cars (signaling heavier demand) new light vehicle sales are smaller. When CPI growth for used cars decreases relative to new car CPI growth, sales are likely to be higher for new vehicles. As far as timing goes, the current trends suggest that auto sales lead normalized used car CPI slightly as it troughed about a year and a half before used car CPI peaked.

Some interesting regressions suggest that a strong negative correlation exists between used car CPI and the monthly price of CarMax. A weaker negative regression can be found between used car CPI and Ford's stock price. This may suggest that KMX stock price moves more strongly with used car CPI changes than the rest of the auto industry, but this conclusion may be all. Due to the reflation of the post-crisis economy, any correlation with a growing stock price can be a bit skewed. In the end, these two statistical connections are probably not significant despite having low p-values.

This article was written using Quantopian's IPython platform. The Python code can be downloaded here: .py .ipynb

|

| Data from Quantopian and Bureau of Economic Analysis |

With sales starting to slow, there has been an incline in inventory that has left the U.S. auto suppliers in a pickle. Overall, production and imports of cars need to be falling to keep the industry in equilibrium in order to maintain a stable price. Domestic production, in the past 12 months, has fallen just over 14.3 percent while the declines in imports from Canada and Mexico are less significant (and very volatile). This conveys an interesting political signal that suggests Trump's domestic manufacturing goals. After demanding U.S. auto companies to move their manufacturing bases inside the country in his first days as the President, these initial data suggest his protests have been futile. Another interesting observation is to note that inventories haven't seen as significant a move as U.S. production has in the last two years. In fact, inventories have always oscillated within 2.0 and 3.0 with only the latest data peaking about 3.0. The abrupt change in inventories could be a drag on prices which, combined with falling sales, could weigh heavily on automakers' bottom lines.

|

| Data from Bureau of Labor Statistics |

From the Bureau of Labor Statistics, consumer price index (CPI) data for automobiles, both used and new can be viewed over the past ten years. The CPI for both used and new vehicles has stayed relatively flat from 2012 to now after recovering from a dip caused by a lapse in demand during the financial crisis. For new and used vehicles, prices recovered above their pre-crisis levels in 2010 with more volatility in used car prices. In fact, it seems as if the most of the fluctuations in the overall auto CPI are caused by movement in used CPI. According to this data, automakers selling new cars have enjoyed stable, increasing prices with used car prices inflated beyond their 2007 levels. Perhaps, over the past six years, this phenomenon led consumers to believe that purchasing a new car over a used car was the smarter decision. Thinking practically, used car demand growth post-crisis makes sense because consumers who needed a vehicle might not have had the discretionary funding to purchase an entirely new car. But as demand strengthened, prices rose, and consumers calmed, new auto sales grew. It is possible that now we are observing demand for the "cheaper" used autos grow replacing demand for new autos. This might explain why U.S. production has trailed off while inventories have continued to rise. It is also interesting to note that, according to Reuters, consumer discounts were $441 higher per vehicle than a year ago, a sign that companies were trying to compete with cheaper used cars on the market.

Post-crisis, an interesting trend in used car CPI and light vehicle sales data can be identified. Using data from 2010 on, one can observe a strong negative correlation between used car CPI and new light vehicle sales as reported by the Bureau of Labor Statistics. With a correlation coefficient of -0.73 and a statistically significant p-value, the data suggests that as used cars get more expensive relative to new cars (signaling heavier demand) new light vehicle sales are smaller. When CPI growth for used cars decreases relative to new car CPI growth, sales are likely to be higher for new vehicles. As far as timing goes, the current trends suggest that auto sales lead normalized used car CPI slightly as it troughed about a year and a half before used car CPI peaked.

Some interesting regressions suggest that a strong negative correlation exists between used car CPI and the monthly price of CarMax. A weaker negative regression can be found between used car CPI and Ford's stock price. This may suggest that KMX stock price moves more strongly with used car CPI changes than the rest of the auto industry, but this conclusion may be all. Due to the reflation of the post-crisis economy, any correlation with a growing stock price can be a bit skewed. In the end, these two statistical connections are probably not significant despite having low p-values.

This article was written using Quantopian's IPython platform. The Python code can be downloaded here: .py .ipynb

Comments

Post a Comment