The Chinese Market Will Never Be the Same

In 2018, President Donald Trump set out on a path to improve the US economy by challenging the US-China trade relationship which he determined was unfairly tilted against the US. Over the past year, tariffs were implemented by both governments as pressure on unresolved trade negotiations for a new deal built. As of the latest round of tariffs, the US will add an additional 10 percent tariff on all Chinese imports after there was no resolution following the previous round (tariff of 25 percent on $200 billion of Chinese exports to the United States and tariffs of up to 25 percent on $60 billion of US exports to the China).

As expected, the aggressive behavior from both sides have created rifts in the various markets included in US-China trade. As of June, Chinese imports of US goods fell 31.4 percent to just $9.4 billion while US imports of Chinese goods fell 7.8 percent to $39.3 billion. The steep decline in US exports to China has caused US companies that previously did business with the Asian giant to face losing access to the consumers of their largest foreign market either by having to pay a steep tariff or not exporting at all.

However, the overarching sentiment is that once a trade deal is agreed up, the channels of business will reopen and return to normal. That is an optimistic scenario indeed. In fact, a longstanding geopolitical desire to decouple from the US combined with an economic imperative is likely to change these markets in perpetuity. The relationship between the two superpowers was long a fragile one, and new strains have allowed the fragility to give way to transformation.

![]()

From a big picture perspective, economic data shows that capital flows into the United States from China has been heavily impacted by the trade uncertainty. A report from Rhodium Group reveals that Chinese capital has nearly dried up as foreign direct investment (FDI) tanked from $46 billion in 2016 to $5 billion in 2018. Chinese purchases of US real estate also plummeted from $30.4 billion to $13.4 billion according to the National Association of Realtors. Capital flows are typically the first to go, so it makes sense to see these markets sensitive to geopolitical rifts. However, the lasting damage is evident in other more specific key markets of physical that have been affected to a similar degree and pose more of a threat to the US economy.

According to Reuters, the trade took some time to develop, but as Chinese consumers became more advanced in their food choices, cherry imports from the US reached $200 million in 2017 up from no trade at all in 2000. Since the peak, importers have recently fled the market though as 50 percent tariffs caused the cherry trade to shrink to about 10 percent of what it was. However, the US importers were not just ignored but likely replaced. In the same article, Reuters pointed out that the Chinese government relaxed regulations and encouraged cherry imports from Central Asia to replace the volume that used to be filled by the US.

Chinese imports of soybeans by country in $USD from Republic of China’s General Administration of Customs

Chinese imports of soybeans by country in $USD from Republic of China’s General Administration of Customs

What’s important to notice is that most of the countries remained robust trading partners with China even when trade negotiations produced a deal to increase Chinese imports from US producers. The data shows that purchasing from the US definitely improved but didn’t come near to what imports were beforehand. There’s a strong possibility that China’s imports of US soybeans may neve reach peak levels. In August 2018, Han Jun, China’s vice agriculture minister, said “If other countries become reliable suppliers for China, it will be very difficult for the U.S. to regain the market.”

Beijing has already begun discussions with Russia to “deepen trade in soybeans” according to RT. These conversations are no doubt meant to put pressure on the United States to ease on the tough trade position or face divided demand in a market it used to dominate. Excess competition will also put pressure on soybean prices exporters as like Russia and other economies continue to make themselves available in trade deals like Russia’s and other’s forged from China’s “Belt and Road” Initiative. The price effect is already evident as soybean futures contracts continue to trade below $900 midway through 2019, down from about $1,040 at the beginning of 2018.

The Oxford Institute for Energy Studies illustrates the US-China energy trade it well in its report, “US-China: The Great Decoupling.” Several US-China energy markets were growing leading up to 2018: liquified petroleum gas (LPG) reached about 1 million b/d in 2017, crude oil imports reached an all-time high of 440,000 b/d in January 2018, US naphtha imports reached about 4.5 percent of total naphtha with rising US production looking to lift it, and natural gas imports were 4 billion cubic meters with hopes those that Chinese demand would continue to increase.

As trade tensions develops, those markets became closed off. LPG imports fell to average 0.5 million b/d, crude imports fell to just 44,000 b/d, and the plans for Chinese refineries to invest in upgrades to take on more US oil and naphtha were delayed. The largest energy consuming economy in the world, accounting for 23.6 percent of the world’s total energy consumption according to BP, was suddenly retreating from US supplies. While it seems like a trade deal might be all that’s needed to resolve the issue, steps are being taken that will have more lasting impacts on the US’s access to Chinese demand.

To replace the US imports, China returned to existing relationships to increase imports from them or form new relationships to countries willing to export. In LPG, China has turned back to the Middle East (including Iran in the face of US sanctions) and even added Argentina, Australia, and Canada as importers. Crude oil imports of heavy crude from the Middle East and other nations who produce that grade are likely to remain favorable to Chinese refineries which will delay capital expenditures spent on adjustments for receiving US light crude.

China will also look domestically for new supply sources. President XI declared in August 2018 the need to address “the issue of supply security.” China recently announced plans to boost oil exploration capital spending by 20 percent to increase domestic production by 50 percent through 2021. The trend has already reversed with production up 0.8 percent in the first five months of 2019, an improvement from the -3.0 percent reduction in production in the first five months of 2018. Like the soybean market, the energy commodity markets will now become crowded with more competition for Chinese demand, and US producers are likely to suffer.

In fact, looking at MIT’s trade data reveals that several of US’s largest exports to China are related to industries highlighted by the initiative:

Overall, these export categories account for 26.87%, or $35.8 billion, of US total exports to China. With the trade tensions in full swing, the Chinese government can put even more emphasis on these goals that promote China’s independence from foreign exports, in particular advanced technology from the US. Uncertainty generated from the potential of further bans of Huawei will also force domestic Chinese technology companies to face inward when looking to expand to new markets especially as consumer spending has been the more reliable source of growth in the Chinese economy.

![]()

Limiting US’s access to the expansive demand in China is part of the larger plan of breaking from the previously intimate US-China relationship. In reducing that relationship, the Asian giant has planned to look to its neighbors as a replacement through the “Belt and Road” initiative. The Chinese-led plan introduced in 2013, called “a hedge strategy against the eastward move of the US” by a retired Chinese general, looks to connect the different Asian regions economically through investments in infrastructure and transportation. In a time with increased geopolitical and economic conflict with the United States, China is likely to advanced projects and relationships like the “Belt and Road” to reduce US access to its robust demand.

Does this mean that the United States’ export relationship with China is over completely? Unlikely. If trade negotiations are resolved, access to the Chinese market should be reinstated and trade will resume. However, US exporters may find it harder to do business there. The markets are likely to be crowded by competition, lost to domestic development in those markets, or closed off by geopolitical uncertainty. No matter the reason, the US economy will feel the effects of reduced competitiveness and less accessibility to the second largest economy in the world, and the effects of the trade war will last long after it ends.

As expected, the aggressive behavior from both sides have created rifts in the various markets included in US-China trade. As of June, Chinese imports of US goods fell 31.4 percent to just $9.4 billion while US imports of Chinese goods fell 7.8 percent to $39.3 billion. The steep decline in US exports to China has caused US companies that previously did business with the Asian giant to face losing access to the consumers of their largest foreign market either by having to pay a steep tariff or not exporting at all.

However, the overarching sentiment is that once a trade deal is agreed up, the channels of business will reopen and return to normal. That is an optimistic scenario indeed. In fact, a longstanding geopolitical desire to decouple from the US combined with an economic imperative is likely to change these markets in perpetuity. The relationship between the two superpowers was long a fragile one, and new strains have allowed the fragility to give way to transformation.

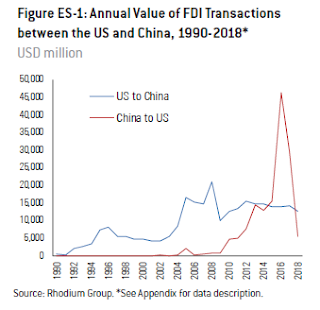

From Rhodium Group

From a big picture perspective, economic data shows that capital flows into the United States from China has been heavily impacted by the trade uncertainty. A report from Rhodium Group reveals that Chinese capital has nearly dried up as foreign direct investment (FDI) tanked from $46 billion in 2016 to $5 billion in 2018. Chinese purchases of US real estate also plummeted from $30.4 billion to $13.4 billion according to the National Association of Realtors. Capital flows are typically the first to go, so it makes sense to see these markets sensitive to geopolitical rifts. However, the lasting damage is evident in other more specific key markets of physical that have been affected to a similar degree and pose more of a threat to the US economy.

Agriculture Imports: Cherries

While China has been known for its massive metal exports and raw commodity productions, the sheer size of its population has forced it to import large amounts of foodstuffs from the US. The US-China cherry trade is one specific example where the deterioration of the trade relation lead to “sky-high tariffs on US cherries” entering China.According to Reuters, the trade took some time to develop, but as Chinese consumers became more advanced in their food choices, cherry imports from the US reached $200 million in 2017 up from no trade at all in 2000. Since the peak, importers have recently fled the market though as 50 percent tariffs caused the cherry trade to shrink to about 10 percent of what it was. However, the US importers were not just ignored but likely replaced. In the same article, Reuters pointed out that the Chinese government relaxed regulations and encouraged cherry imports from Central Asia to replace the volume that used to be filled by the US.

Agriculture Imports: Soybeans

While the cherry market appears small, a similar trend in the larger US-China soybean market can be identified that has more significant implications for US farmers. Chinese customs data show that imports of US soybeans have fallen drastically in the past year and a half. In January 2018, $2.45 billion worth of soybeans entered China before tariffs pushed that to a low of around $30 million by the end of the year, a decrease of over 95 percent. This lead to significant changes in imports from various countries: Chinese imports of soybeans by country in $USD from Republic of China’s General Administration of Customs

Chinese imports of soybeans by country in $USD from Republic of China’s General Administration of Customs- Imports from Brazil spiked from about $868 million in January 2018 to almost $4 billion by May 2018.

- Imports from Argentina peaked from very little to $231 million in August 2018.

- Imports from Russia initially fell but picked up again in late 2018 reaching above $30 million by October 2018.

- Imports from Kazakhstan even saw a boost in early 2018 and early 2019 reaching $2.3 million in May 2019.

What’s important to notice is that most of the countries remained robust trading partners with China even when trade negotiations produced a deal to increase Chinese imports from US producers. The data shows that purchasing from the US definitely improved but didn’t come near to what imports were beforehand. There’s a strong possibility that China’s imports of US soybeans may neve reach peak levels. In August 2018, Han Jun, China’s vice agriculture minister, said “If other countries become reliable suppliers for China, it will be very difficult for the U.S. to regain the market.”

Beijing has already begun discussions with Russia to “deepen trade in soybeans” according to RT. These conversations are no doubt meant to put pressure on the United States to ease on the tough trade position or face divided demand in a market it used to dominate. Excess competition will also put pressure on soybean prices exporters as like Russia and other economies continue to make themselves available in trade deals like Russia’s and other’s forged from China’s “Belt and Road” Initiative. The price effect is already evident as soybean futures contracts continue to trade below $900 midway through 2019, down from about $1,040 at the beginning of 2018.

Energy Imports

The emergence of the United States as a new energy producing power provided an opportunity for it to bolster its economy with the opportunity to become an exporter of energy commodities. The US reached new all-time highs in the production of natural gas, 2,791 bcf in March 2019, and crude oil, 12.1 million b/d in April 2019, with hope that it would have access to the largest markets in the world, its own, the EU, and China. Major steps to becoming an exporting power were well off, but producers of raw energy commodities and products were making considerable headway in the Chinese market before tariffs.The Oxford Institute for Energy Studies illustrates the US-China energy trade it well in its report, “US-China: The Great Decoupling.” Several US-China energy markets were growing leading up to 2018: liquified petroleum gas (LPG) reached about 1 million b/d in 2017, crude oil imports reached an all-time high of 440,000 b/d in January 2018, US naphtha imports reached about 4.5 percent of total naphtha with rising US production looking to lift it, and natural gas imports were 4 billion cubic meters with hopes those that Chinese demand would continue to increase.

As trade tensions develops, those markets became closed off. LPG imports fell to average 0.5 million b/d, crude imports fell to just 44,000 b/d, and the plans for Chinese refineries to invest in upgrades to take on more US oil and naphtha were delayed. The largest energy consuming economy in the world, accounting for 23.6 percent of the world’s total energy consumption according to BP, was suddenly retreating from US supplies. While it seems like a trade deal might be all that’s needed to resolve the issue, steps are being taken that will have more lasting impacts on the US’s access to Chinese demand.

To replace the US imports, China returned to existing relationships to increase imports from them or form new relationships to countries willing to export. In LPG, China has turned back to the Middle East (including Iran in the face of US sanctions) and even added Argentina, Australia, and Canada as importers. Crude oil imports of heavy crude from the Middle East and other nations who produce that grade are likely to remain favorable to Chinese refineries which will delay capital expenditures spent on adjustments for receiving US light crude.

China will also look domestically for new supply sources. President XI declared in August 2018 the need to address “the issue of supply security.” China recently announced plans to boost oil exploration capital spending by 20 percent to increase domestic production by 50 percent through 2021. The trend has already reversed with production up 0.8 percent in the first five months of 2019, an improvement from the -3.0 percent reduction in production in the first five months of 2018. Like the soybean market, the energy commodity markets will now become crowded with more competition for Chinese demand, and US producers are likely to suffer.

Technology Manufacturing Imports

In a less direct manner of limiting US imports into China, Beijing began a “Made in China 2025” initiative in 2015 that looked to encourage manufacturing in several industries: electric cars and other new energy vehicles, next-generation information technology (IT) and telecommunications, advanced robotics, artificial intelligence, agricultural technology, aerospace engineering, new synthetic materials, advanced electrical equipment, emerging bio-medicine, high-end rail infrastructure, and high-tech maritime engineering. Several industries are listed, but they all have the common theme of being touched by cutting edge technology which is largely dominated by the US.In fact, looking at MIT’s trade data reveals that several of US’s largest exports to China are related to industries highlighted by the initiative:

- Planes, Helicopters, Spacecraft (10%, $13.4 billion)

- Cars (8.7%, $11.5 billion)

- Integrated Circuits (5.8%, $7.75 billion)

- Medical instruments (1.8%, $2.4 billion)

- Computers (0.57%, $758 million)

Overall, these export categories account for 26.87%, or $35.8 billion, of US total exports to China. With the trade tensions in full swing, the Chinese government can put even more emphasis on these goals that promote China’s independence from foreign exports, in particular advanced technology from the US. Uncertainty generated from the potential of further bans of Huawei will also force domestic Chinese technology companies to face inward when looking to expand to new markets especially as consumer spending has been the more reliable source of growth in the Chinese economy.

Breaking From the United States

Limiting US’s access to the expansive demand in China is part of the larger plan of breaking from the previously intimate US-China relationship. In reducing that relationship, the Asian giant has planned to look to its neighbors as a replacement through the “Belt and Road” initiative. The Chinese-led plan introduced in 2013, called “a hedge strategy against the eastward move of the US” by a retired Chinese general, looks to connect the different Asian regions economically through investments in infrastructure and transportation. In a time with increased geopolitical and economic conflict with the United States, China is likely to advanced projects and relationships like the “Belt and Road” to reduce US access to its robust demand.

Does this mean that the United States’ export relationship with China is over completely? Unlikely. If trade negotiations are resolved, access to the Chinese market should be reinstated and trade will resume. However, US exporters may find it harder to do business there. The markets are likely to be crowded by competition, lost to domestic development in those markets, or closed off by geopolitical uncertainty. No matter the reason, the US economy will feel the effects of reduced competitiveness and less accessibility to the second largest economy in the world, and the effects of the trade war will last long after it ends.

This comment has been removed by a blog administrator.

ReplyDelete