Global Liquidity Squeeze Has Weighed on Manufacturing: A BIS Presentation

On May 14th, 2019, Hyun Song Shin, Economic Adviser and Head of Research at the Bank of International Settlements gave a presentation titled "What is Behind the Recent Slowdown?" His presentation presents an explanation on the global slowdown in manufacturing and trade and how the current economic environment has brought about a slowdown in activity.

Shin points out that manufacturing and trade have been a major drag over the past year with European countries seeing their purchasing managers' indices (PMIs) peak in the beginning of 2018 and continue downwards into 2019. A similar trend can be seen in the US's PMI which saw its last April value come in below expectations. China's national PMI reading saw a slightly positive recovery in February but still remains relatively depressed like Europe and the US. Shin also points out this trend of weakened manufacturing is secular from domestic areas of growth like services and employment, particularly in Europe.

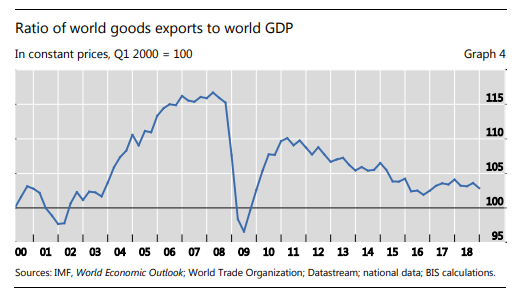

In a world with more protectionism, a slowdown in global trade seems likely to happen especially when two of the most connected trading nations are feuding. Shin suggests that a break down in global value chains (GVC) is the leading cause of a slowdown in manufacturing. He demonstrates this through the tracking of the ratio of world goods exports to world GDP. The data shows that a reversal immediately after the financial crisis has seen global trade decline even before trade tensions became a geopolitical issue.

The decline could also be linked to monetary tightening masquerading as policy normalization which was an inevitable response to the drastic measures taken post-financial crisis. The BIS presentation points out that 65 percent of trade is financed by the firms doing business, in particular, " by the seller in the form of “open account financing” or by the buyer paying upfront in a “cash-in-advance” purchase." These capital intensive processes need active short-term liquidity or they can contract quickly.

So what connects the GVCs in their financing? The BIS found that in "around 80% of bank trade financing was denominated in US dollars" leaving long, interconnected GVCs vulnerable to US dollar trends. In fact, further investigation found that the measure of global trade activity (exports-to-GDP) showed an inverse relationship with movement in the US dollar. Through this relationship, Shin concluded that "globally, high corporate leverage has emerged as a source of vulnerability for growth" because most balance sheets hold dollar-denominated debt which has been sensitive to the strong dollar trend.

In general, the presentation concludes that the struggles to sustain manufacturing growth have come through inefficiencies in capital financing from the banking sector. Relatively weak lending growth after the global financial has hindered GVCs making them less effective. Overall, it has resulted in leveraged corporate balance sheets that force companies to be less expansive in operations making faster growth tougher to achieve.

In a world with more protectionism, a slowdown in global trade seems likely to happen especially when two of the most connected trading nations are feuding. Shin suggests that a break down in global value chains (GVC) is the leading cause of a slowdown in manufacturing. He demonstrates this through the tracking of the ratio of world goods exports to world GDP. The data shows that a reversal immediately after the financial crisis has seen global trade decline even before trade tensions became a geopolitical issue.

The decline could also be linked to monetary tightening masquerading as policy normalization which was an inevitable response to the drastic measures taken post-financial crisis. The BIS presentation points out that 65 percent of trade is financed by the firms doing business, in particular, " by the seller in the form of “open account financing” or by the buyer paying upfront in a “cash-in-advance” purchase." These capital intensive processes need active short-term liquidity or they can contract quickly.

So what connects the GVCs in their financing? The BIS found that in "around 80% of bank trade financing was denominated in US dollars" leaving long, interconnected GVCs vulnerable to US dollar trends. In fact, further investigation found that the measure of global trade activity (exports-to-GDP) showed an inverse relationship with movement in the US dollar. Through this relationship, Shin concluded that "globally, high corporate leverage has emerged as a source of vulnerability for growth" because most balance sheets hold dollar-denominated debt which has been sensitive to the strong dollar trend.

In general, the presentation concludes that the struggles to sustain manufacturing growth have come through inefficiencies in capital financing from the banking sector. Relatively weak lending growth after the global financial has hindered GVCs making them less effective. Overall, it has resulted in leveraged corporate balance sheets that force companies to be less expansive in operations making faster growth tougher to achieve.

Comments

Post a Comment