Oil Prices and Real Interest Rates: An IMF Paper

One of the great economic conundrums of today that continues to stump economists across the globe is the failure of low oil prices to spark a consumption-based boom. Lower prices are supposed to stimulate more demand from the average consumer and lift economies with a boost in sales. Across almost all sectors, firms see their input costs decreasing, especially the transportation and industrial sectors. Consequently, the availability of extra capital allows business and residential investment to increase and offset the losses in the energy industry. Finally, the total gross domestic product rises. This theoretical flow-chart can be followed by most college economic students and has much power for policymakers across the globe.

The question still stands, though, why hasn't the low price of oil supported growth? Average quarterly global GDP growth slowed to 1.98% in 2015, down from 2.50% in 2014 and 2.46% in 2013. The average yearly price of crude oil in both of those years was significantly lower compared to 2015. A glut slashed the WTI spot price by about half from $97.98 and $93.17 in 2013 and 2014 to $48.66 just last year. The data refutes the economic framework first discussed while introducing a fresh inquiry into the dynamics of energy prices and growth. Almost eight months after a staff discussion at the International Monetary Fund forecasted growth in GDP because of the low oil price, their economists have written a paper as to why they were wrong. The aptly named article, "Oil Prices and the Global Economy: It's Complicated," appears to be the answer that economists were looking for with an explanation not easily scripted in a fancy headline as most would hope it to be.

Click here to access the IMF article.

The paper starts out introducing the glut, something that the articles on this blog do often. WTI and Brent price trends including how far they have dropped from June 2014 are cited, but the IMF paper mentions a currency-adjusted price decline. Because of the "20 percent dollar appreciation," the real price change lingers around $60, still a significant sum. Nevertheless, there still remains an interesting currency dynamic that should be analyzed. The price weakness coupled with the dollar appreciation has resulted in emerging, oil exporting markets to be hurt more than usual. From their perspective, their revenue has been discounted while the real value of their debt increased.

The stronger dollar could also be blamed for intensifying the bearish trend of oil prices. As foreign currencies were being devalued, they could afford less and less oil because most of the commodity were being sold on markets with a dollar-denominated price. Nevertheless, the economic downturn cannot be blamed solely on the appreciation of the dollar. The trend only exacerbated the effects of the glut on the price of oil and deflation.

The authors at the IMF continue to reinforce their belief that low oil prices should be a "net plus" for the world's economy because "consumers in oil-importing regions such as Europe have a higher marginal propensity to consume out of income than those in exporters such as Saudi Arabia." This point makes sense, especially in a low-interest-rate environment. The average citizen of a Western country like the United States or a euro nation has an incentive to spend now because they will not earn as much interest on their savings. The only problem with this statement is that it fails to consider the United States as any less of an oil importer despite its new status as the third largest world producer. The low oil price destroyed the stock price of many energy companies who had recently gone shopping for cheap loans. The junk bond market, composed of this debt, saw a decline as a result. The IMF economists, perhaps, underestimate the effect that a faltering energy sector had on the U.S. and the global economy. Cuts of billions of dollars in the United States were part of a 22% drop in global oil and gas investments in 2015. Rystad Energy also predicts another 12% drop in 2016.

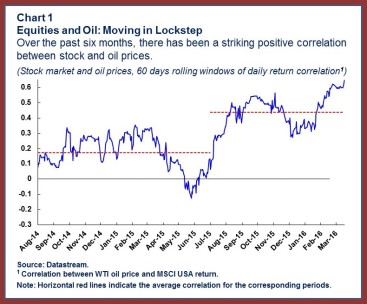

Their first chart describes the bearish relationship quite well and corroborates the argument that business investment had a significant effect on the economy. The blue line shows the correlation between the WTI spot price and U.S. equities.

The article doesn't stop to blame a drop in business investment and continues its discussion with interest rates. Compared to past periods of supply shocks, this glut that began in 2014 was unique because of the low-interest rate environment in which it formed. The next few paragraphs discuss the trend in demand for oil exporters and oil importers. Nothing seems out of the ordinary as oil exporters are forced to cut investment spending with rising risk. Oil importers are set to wait for an increase in consumption and, consequently, a jump in demand to remedy the low oil price. But that jumpstart never came, and oil firms are looking at less demand and more supply for awhile. Here's why.

The problem is that "falling oil prices, this time, coincide with a period of slow economic growth—so slow that the major central banks have little or no capacity to lower their monetary policy interest rates further to support growth and combat deflationary pressures." As my macroeconomics professor says, "The Fed doesn't have enough water in their squirt gun." These explanations adequately sum up the disparaging situation global macroeconomic leaders find themselves in, but a deeper analysis is more beneficial

The authors mention Michael Bruno and Jeffrey Sachs who showed that oil supply shocks cause stagflation when prices go up. Conversely, the IMF economists say that lower prices should do the opposite "lower production costs, more hiring, and reduced inflation." So what did the central banks do wrong this time? The deflationary pressure that is caused by shrinking oil prices indirectly raises real interest rates. This follows from the formula for real interest rates which is calculated by subtracting inflation from the nominal interest rates (interest rates set by central banks). In short, deflation can act as a rise in interest rates if the central banks do not adjust nominal interest rates down as well. This time around, they cannot because rates are already at zero (or sub-zero if you're Japan). Higher interest rates, as a result, have a pro-cyclical effect on the global economy where "compressed demand" and "stifled output and employment" are the result. The observation is not too complicated but operates on a rule found deep in a macroeconomics textbook.

And that's really the gist of it. The drop in oil prices has had a pro-cyclical macroeconomic effect as a result of an inability to reduce interest rates. The IMF authors conclude saying that "the current episode of historically low oil prices could ignite a variety of dislocations including corporate and sovereign defaults." The dangers are real and could change the landscape of the energy market. Higher real interest rates explain the failure of the junk bond market, and why investors sold off debt in 2015. Companies that need new funding will now have to deal with higher risk premiums, including Exxon-Mobil which has recently seen its AAA rating in danger. The solution seems dim. Because interest rates are so low, central banks have no choice but to let the cycle continue without cushioning it. Then, interest rates will go up rapidly. The Fed clearly acknowledges this real interest rate increase as the problem and continues on its path of waiting.

My brief analysis of this IMF paper is just the tip of the iceberg. I encourage all my readers to read the primary source and continue researching the ideas from the paper. The research is excellent and, for the most part, eye-opening. An understanding of the underlying macroeconomic trends in this interesting economic environment can only help an investor in the long run.

The question still stands, though, why hasn't the low price of oil supported growth? Average quarterly global GDP growth slowed to 1.98% in 2015, down from 2.50% in 2014 and 2.46% in 2013. The average yearly price of crude oil in both of those years was significantly lower compared to 2015. A glut slashed the WTI spot price by about half from $97.98 and $93.17 in 2013 and 2014 to $48.66 just last year. The data refutes the economic framework first discussed while introducing a fresh inquiry into the dynamics of energy prices and growth. Almost eight months after a staff discussion at the International Monetary Fund forecasted growth in GDP because of the low oil price, their economists have written a paper as to why they were wrong. The aptly named article, "Oil Prices and the Global Economy: It's Complicated," appears to be the answer that economists were looking for with an explanation not easily scripted in a fancy headline as most would hope it to be.

Click here to access the IMF article.

The paper starts out introducing the glut, something that the articles on this blog do often. WTI and Brent price trends including how far they have dropped from June 2014 are cited, but the IMF paper mentions a currency-adjusted price decline. Because of the "20 percent dollar appreciation," the real price change lingers around $60, still a significant sum. Nevertheless, there still remains an interesting currency dynamic that should be analyzed. The price weakness coupled with the dollar appreciation has resulted in emerging, oil exporting markets to be hurt more than usual. From their perspective, their revenue has been discounted while the real value of their debt increased.

The stronger dollar could also be blamed for intensifying the bearish trend of oil prices. As foreign currencies were being devalued, they could afford less and less oil because most of the commodity were being sold on markets with a dollar-denominated price. Nevertheless, the economic downturn cannot be blamed solely on the appreciation of the dollar. The trend only exacerbated the effects of the glut on the price of oil and deflation.

The authors at the IMF continue to reinforce their belief that low oil prices should be a "net plus" for the world's economy because "consumers in oil-importing regions such as Europe have a higher marginal propensity to consume out of income than those in exporters such as Saudi Arabia." This point makes sense, especially in a low-interest-rate environment. The average citizen of a Western country like the United States or a euro nation has an incentive to spend now because they will not earn as much interest on their savings. The only problem with this statement is that it fails to consider the United States as any less of an oil importer despite its new status as the third largest world producer. The low oil price destroyed the stock price of many energy companies who had recently gone shopping for cheap loans. The junk bond market, composed of this debt, saw a decline as a result. The IMF economists, perhaps, underestimate the effect that a faltering energy sector had on the U.S. and the global economy. Cuts of billions of dollars in the United States were part of a 22% drop in global oil and gas investments in 2015. Rystad Energy also predicts another 12% drop in 2016.

Their first chart describes the bearish relationship quite well and corroborates the argument that business investment had a significant effect on the economy. The blue line shows the correlation between the WTI spot price and U.S. equities.

The article doesn't stop to blame a drop in business investment and continues its discussion with interest rates. Compared to past periods of supply shocks, this glut that began in 2014 was unique because of the low-interest rate environment in which it formed. The next few paragraphs discuss the trend in demand for oil exporters and oil importers. Nothing seems out of the ordinary as oil exporters are forced to cut investment spending with rising risk. Oil importers are set to wait for an increase in consumption and, consequently, a jump in demand to remedy the low oil price. But that jumpstart never came, and oil firms are looking at less demand and more supply for awhile. Here's why.

The problem is that "falling oil prices, this time, coincide with a period of slow economic growth—so slow that the major central banks have little or no capacity to lower their monetary policy interest rates further to support growth and combat deflationary pressures." As my macroeconomics professor says, "The Fed doesn't have enough water in their squirt gun." These explanations adequately sum up the disparaging situation global macroeconomic leaders find themselves in, but a deeper analysis is more beneficial

The authors mention Michael Bruno and Jeffrey Sachs who showed that oil supply shocks cause stagflation when prices go up. Conversely, the IMF economists say that lower prices should do the opposite "lower production costs, more hiring, and reduced inflation." So what did the central banks do wrong this time? The deflationary pressure that is caused by shrinking oil prices indirectly raises real interest rates. This follows from the formula for real interest rates which is calculated by subtracting inflation from the nominal interest rates (interest rates set by central banks). In short, deflation can act as a rise in interest rates if the central banks do not adjust nominal interest rates down as well. This time around, they cannot because rates are already at zero (or sub-zero if you're Japan). Higher interest rates, as a result, have a pro-cyclical effect on the global economy where "compressed demand" and "stifled output and employment" are the result. The observation is not too complicated but operates on a rule found deep in a macroeconomics textbook.

And that's really the gist of it. The drop in oil prices has had a pro-cyclical macroeconomic effect as a result of an inability to reduce interest rates. The IMF authors conclude saying that "the current episode of historically low oil prices could ignite a variety of dislocations including corporate and sovereign defaults." The dangers are real and could change the landscape of the energy market. Higher real interest rates explain the failure of the junk bond market, and why investors sold off debt in 2015. Companies that need new funding will now have to deal with higher risk premiums, including Exxon-Mobil which has recently seen its AAA rating in danger. The solution seems dim. Because interest rates are so low, central banks have no choice but to let the cycle continue without cushioning it. Then, interest rates will go up rapidly. The Fed clearly acknowledges this real interest rate increase as the problem and continues on its path of waiting.

My brief analysis of this IMF paper is just the tip of the iceberg. I encourage all my readers to read the primary source and continue researching the ideas from the paper. The research is excellent and, for the most part, eye-opening. An understanding of the underlying macroeconomic trends in this interesting economic environment can only help an investor in the long run.

Comments

Post a Comment