The Question Every Investor Is Asking

After a long hard day at work, an investor finds himself retreating to his home office to check on his own investments. Sitting beside the dusty keyboard and piles of notepads scrawled with calculations and stock symbols, a magic lamp sits crested by the soft glow of his desktop computer with three monitors. He rubbed the side because that's what everyone is supposed to do when they come across one of these. A phantasmic figure appeared, filling his office, and said, "I shall grant you one answer to any question about the markets." The tired trader slumped in his chair thinking, then finally asked, "Where is the bottom in this crude oil market?"

Now if you were hoping for an answer then you are among the millions of financial professionals that would ask that same question. Just about everyone has contributed their own opinions on when oil prices will reclaim their hefty price tag (including me), but just about everyone has been wrong at least once. I can remember reading tons of articles last year projecting $60 a barrel oil by the end of 2015. Now, it's almost half of that. So research and calculations continue with the disturbing thought that the rebound could creep up on anyone, and anyone could lose out on the opportunity to cash in.

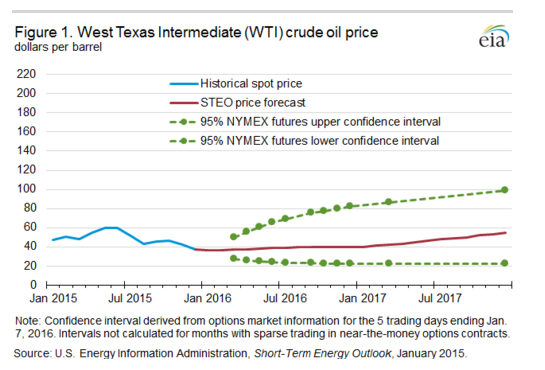

Perhaps one of the most important vehicles of crude oil prediction is the U.S. government's own Energy Information Agency, This blog has used its data and analysis many times before, and it will continue to endorse it as one of the analytical strongholds of the glut. Weekly, the agency produces a report called This Week In Petroleum which lists supply estimates for the week and interesting figures that show the current state of the domestic energy market. Major news outlets use this agency in its articles about the crude market which translates to price movement in response to the EIA's opinions. Last month, this chart was posted showing their calculated projections for the next two years. In 2016, WTI prices are forecasted at an average of $38 a barrel with Brent at $40 a barrel. A year after that, WTI prices should average $47 a barrel and Brent $50 a barrel. With those $60 projections out the window and the relentless pumping of non-OPEC producers, speculators are expecting saturated markets for longer. As we saw in the current ratios of S&P oil and gas companies, the energy industry is opting for more liquidity with the expectation that prices will weigh on revenue. Their outlook is supported by the EIA's prediction that 700,000 barrels will be added to inventories in the current year. The first draw on inventories isn't expected until the third quarter of 2017,

But we don't care about when prices are getting better if we already know that's going to happen. The true profits come when traders abide by the simple rule "buy low, sell high." If you just found your interest in this article again, the EIA has something for you too. In the weekly report released Wednesday, the focus highlights crude stocks in most saturated regions of the United States. Stocks in the Gulf Coast approached 256 million barrels and stocks in Cushing, Oklahoma set a new record of 65 million barrels just two weeks ago. Any seasonal oil trader knows that inventories typically top in January and February due to refinery maintenance, but that doesn't relax any pressures on the market. In fact, the pressure on oil storage capacity is only rising. With these conditions, expectations for future prices continue to be depressed especially with an increase in Iranian oil considered a sure thing. In comes the term contango, a concept that could help understand where this bottom is.

A market is considered in contango when the expected futures price is higher than the current spot price. The orange line, which shows WTI contracts from April 2016 to April 2017, is an example of this type of market shape. While it appears similar to a normal futures curve, contango markets are different because the futures price is expected to converge to the current spot price. Because of this dynamic, speculators can buy oil at a cheaper price now while hedging that same oil by selling a futures contract at a higher price. A similar process happened in late 2008 and 2009 when the WTI market was in contango by about $15 a barrel. In the market now, futures prices 12 months ahead have slipped to about $10 a barrel in contango. From February 1st to the 23rd, the EIA reported a spread of about $10.44 a barrel while citing that buying and storing oil does "not typically become economical until contango reaches $10-$12/b." But what does that mean for the bottoming of oil prices? The answer is in the price for oil storage capacity. With stocks consistently rising, capacity will continue to fill up and supply will get tighter. Because most analysts believe that U.S. producers will continue to pump what they can, demand will remain stable. Thus, speculators looking to make a profit of the contango situation will see storage costs increase. When this happens, Financial Times's John Dizard says "peak bear" in oil is close. He projects a "much more rapid rise in spot price in the coming months" because of an unwinding of oil cash-and-carry positions. The precipitation of the gains should occur when storage and the construction of new storage slow down significantly, and this could come relatively soon per the EIA's reported 84% and 89% capacity utilization rates in the Gulf Coast and Cushing respectively. Pressure may also come from a rising spot price that would flatten the curve altogether. As the market begins to stabilize, a convergence towards the yearly average represented by the dotted line would end the contango shape and result in a liquidation of positions.

Dizard's article refers to a quote from the President of Rosewood Trading that said, "...when contangos unwind, they move very fast...I would say this will happen within a six-month period." Again, market timing is brought up here with predictions of an uptrend in a half a year, but it's important to remember how quick things can change, in both directions. The unruly market has already misdirected thousands of investors because its saturation of uncertainty. The unwinding of a contango market could occur soon but may prove to be unsustainable as a trend. It's important to monitor capacity utilization and inventories in order to recognize a false bottom if one forms (like in early 2015). A contango situation could resume after a strong recovery if fundamentals don't improve and the rent for empty storage tanks drop in price. Interest rate hikes (or the lack thereof) may also affect cash-and-carry positions as they increase the cost of getting the capital to rent the tanks. Low rates could translate to more contango while a few hikes signal the bottom.

The genie might not be clear with his answer, and if his name is John Dizard, he might not even be that accurate at all. However, a contango market can be quite telling. The unwinding of the contango crude market in 2009 led to some of the highest prices ever seen. While the 2015 and 2016 contango market is not as extreme, its length is much longer. The accumulation of carry positions over this time could lead to a bottom and then a rebound, shooting the sprice up to its 2015 yearly average of $42.98 in the graph above. For that reason, following the shape of the oil futures curve can provide us with some insightful information...and something to do in place of looking for that golden lamp.

Comments

Post a Comment