In the last week of August, the investing world experienced a significant correction that saw the exit of large amounts of money from the market. The reason for this event was the development of a speculation based bubble as traders traded on an economy that was weaker than sentiment that surrounded it. The markets could not support this extra girth and dropped it. The cyclicality of the business model begs for economists and long-term investors to give attention to macroeconomic dynamics. Specifically, analyzing the accuracy of the efficient market hypothesis can be the key to creating and exiting positions based on speculative bubbles. Are prices at any point in time accurate depictions of supply and demand fundamentals? Or are price movements the result of the psychological chaos that is investor sentiment? At the beginning of the millennium, the market saw a reevaluation of stock prices that were inflated by the seemingly revolutionary sentiment behind tech stocks. The dot com boom of the early 1990’s building into 2000 and 2001 can be compared to the recent correction the record high Dow Jones that survived a volatile first and second quarter in 2015, but ultimately fell because of a hollow economic recovery signaled by Chinese weakness. Separated by a period of fifteen years, short-term business fluctuations saw two crests and two troughs (2001 and 2008) in this frail era of an increasingly complex financial system. The dot com bubble formed after Greenspan’s Era of Moderation where monetary policy encouraged riskier investing in stocks and eventually tech stocks that seemed to rise forever. Dot com securities reached their peak in March of 2000 where they tumbled in a matter of days. The following year brought recession like symptoms as pensions and other major investment funds had made their move to stocks as they were deemed the safest (just like real estate in 2008).

|

DJIA 2015

|

| DJIA 2001 |

|

Looking at the six month charts, we can see the periods leading up to that Dow Jones crashes as a result of speculative bubbles in 2000-2001 and 2015. Both major drops are over 30% and backed with intense volume data. Another technical similarity is the amount of time drops of over 1000 points took to reach their bottoms, both in less than two weeks. The brevity of the sell-offs spells out how dangerous corrections can be to anyone’s portfolio. Just as the characteristics of the drop are similar, the retracements immediately following the bottom can be compared as well. Retracements that occur this quickly are typically the result of long positions being made as resistance levels are established across the market. These “stable” signs of tapering off volatility inform traders that the correction has found a value acceptable to the fundamental situation. Therefore, it is also important to note the lengths of volatile movement that precede the surety of the drop. Now that we’ve realized a connection between the dot com correction in 2001 and the Chinese correction in 2015, I’d like to observe WTI price movement in order to gain insight on the ambiguities in the energy markets today.

|

WTI 2015

|

|

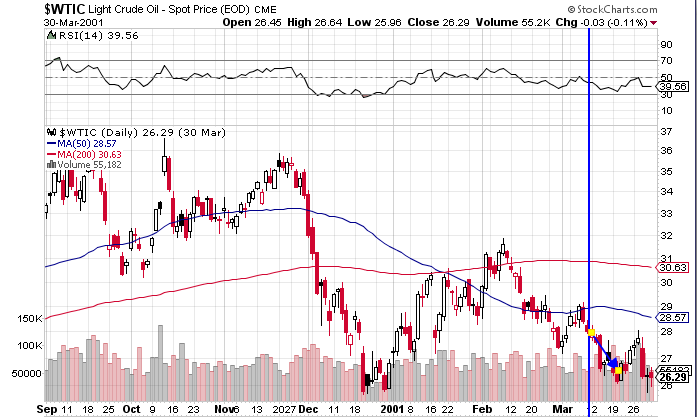

WTI 2001

|

It may seem frivolous to look at charts that don’t appear to be related to the technology bubble, but we may be able to make observations about the overall economy’s reaction to the bubble. One similarity can be seen in the short term reaction to the speculative bubble popping. After a week or two of futures trading, a small sell-off can be seen tacked on to movement from before the dip. Before this small period, movement does not lend itself to a comparison. Although a 50-day moving average suggests similar movement, the patterns are actual very different for an obvious reason. Despite the fact that stocks were overvalued in both situations, the 2015 crash was part of an ongoing complication in crude oil supply, a major glut that had sent prices through the floor. WTI downward trends in 2001 may only be a result of demand data that was influenced by the recession following the tech crash. The resulting volatility inspired a sell-off. Crude oil movements in 2014-2015 are supply related with long-term volatility and stable short term directions (except as of September). Another difference may further insight into the relationship between equities and commodities prices. The onset of inflationary or deflationary environments can change how the two securities are correlated. In inflationary settings, commodities and stocks move together reacting to an increase in exports and a strong economy. Deflationary environments cause stocks and commodities to move against each other as they react to currency strength differently. In 2001, investors are going to be trading in an inflationary period so when stocks are dipping so are crude oil futures. The economy we are trading in now is almost deflationary causing a relationship to fizzle. Investors have seen with the stronger dollar, commodities are hurt but stocks are encouraged by the possibility of a stronger economy. In the comparison between the tech stock bubble of 2001 and the recent bubble in 2015, we have been able to tease out some factors that can be identified through the similarities and differences of the two periods. It is apparent that a short term loss in commodities is the result of any speculative bubble popping, but the formation of a stock bubble does not dictate commodity movement (or at least WTI crude oil movement). Instead, attention should be paid to the macroeconomic condition of inflationary and deflationary pressures as well as unique fundamental atmospheres. For now, we can conclude that the effects of the correction on WTI are over, and supply fundamentals as well as deflationary pressures will define the future movement of the most watched energy commodity.

Comments

Post a Comment